International Association Backs Strong Market

STORY INLINE POST

Q: What is your view of the aviation industry in Mexico and the main changes in the market since 2016?

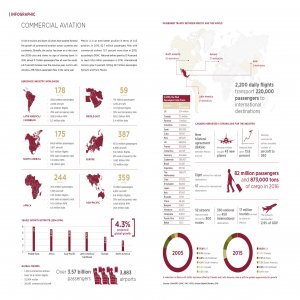

A: In Mexico, the aviation industry contributes positively to the national economy, generating more than 1 million direct and indirect jobs and contributing 3 percent to the national GDP. This represents more than US$35 billion annually and reflects the importance of aviation for Mexico.

The Mexican aviation industry has entered a consolidation stage. The variety of airline business models have found their market niches, maximizing the transport of passengers in the country. Airline offering includes legacy carriers, hybrid, low-cost and ultra-low cost, in addition to regional aviation. An important element of the positive results is the solid commitment driving the development of new routes and flows to maximize connectivity. Additionally Mexican airlines are entering a new era through joint cooperation models such as that recently implemented between Delta Airlines and Aeroméxico. We are likely to see additional strategic alliances that will drive potential consolidations or mergers in the future.

Q: What are IATA’s expectations for the passenger and cargo market in the country during 2017?

A: The passenger market in Mexico is strong and has registered robust growth for a number of years. We expect passenger growth to reach 4 percent this year in Mexico. In terms of the freight market, we do not have specific numbers for Mexico but in the first half of 2017, airlines in Latin America saw an increase in demand of 9.8 percent. Nevertheless, volumes remain 10 percent lower than at their peak in 2014.

Q: What challenges does the aviation sector face in Mexico?

A: The sector has an enormous opportunity for growth and consolidation; the biggest challenges will come from over-onerous taxation, airport infrastructure, operating costs and a stable regulatory framework. Air transport needs smart regulation, efficient operations and technology and most importantly, the adoption of best international practices to maximize the benefits of the sector.

With hundreds of major airlines operating all over the world, airlines are used to competing among themselves by offering excellent services to a wide range of customers at attractive prices. The biggest challenge airlines face in Mexico is more related to the country’s aviation policies. Recently, we have seen a flurry of perhaps well-intentioned, yet misguided, legislation that is out of sync with global best practices and that is damaging air transport in Mexico.

Legislation mandating free checked bags, nonsequential coupon use and free ticket cancellations up to 24-hours before the flight prevent airlines from maintaining competitive prices or even being able to service some routes. Close consultation between the authorities, airlines and other key stakeholders is needed to ensure aviation policy is aligned with global best practices and does not damage Mexico’s budding, yet fragile, air transport industry.

Q: What are the most important trends you are seeing in the aviation market?

A: Airlines have made major efforts to make flying more affordable. Thus, more passengers are traveling today than 10 or 20 years ago. The average roundtrip ticket price has fallen 64 percent since 1996 and this has democratized air travel. In Latin America, air travel is accessible for more people than ever and this is one of the reasons why we expect the number of passengers to double between 2015 and 2035. It is up to governments to ensure airports and other vital pieces of air infrastructure are in place so airlines can serve this demand.

Another trend that has transformed the industry and the passenger experience is technology. More and more aspects of the passenger journey are controlled by the passenger, from check-in to baggage tracking, in addition to other services from a smartphone. We expect technology to facilitate further improvements for passengers and usher in changes at airports as well that could speed up security processes and allow boarding with automated access gates, for example.

Q: How would you describe the current status of Mexican airlines and airports in comparison to the rest of the Americas?

A: Generally speaking, Latin American carriers are doing a superb job and the market has been supportive in terms of growth. The airlines’ corporate strategy and discipline have boosted the sector and carriers co-exist amid intense competition. The region is emerging in recent years with new models of operations, consolidations, mergers and strategic alliances. States must continue facilitating the development of the aviation industry. There is a market of more than 600 million people with an average growth per year of 8 percent so without a doubt the potential is enormous. But States must work to modernize airport infrastructure, control operating costs, adopt international best practices and apply smart regulation.

Only by adapting these policies will airlines be able to absorb this market growth. The main airports in the region must be able to handle large volumes of point-to-point and connecting passengers through efficient mechanisms that allow airlines to invest in their development with a long-term vision, respecting the airlines' financial health but also passenger rights, and in security schemes while avoiding the pitfalls of an overregulated market. Given operational, capacity and cost conditions, the region has the potential to double its aviation industry in the next 15 years.

Q: Which areas should be strengthened to support the growth of aviation in Mexico?

A: The areas that should be strengthened are overall airport infrastructure, slot regulation aligned to international best practices, technology that allows efficient processes and smart regulation. This not exclusive to Mexico or any other specific country in the region.

Q: What steps is IATA implementing to guide its airlines to adhere or subscribe to environmental practices?

A: The airline industry was the first industry to make commitments on its own to reduce carbon emissions with a calendar for reducing our carbon footprint. Our industry has a four-pillar strategy on climate change, comprising improvements in technology, operations and infrastructure.

In addition, we have supported the implementation of the Carbon Offsetting Scheme for International Aviation (CORSIA), in which aircraft operators will be required to purchase offsets, or “emission units,” for the growth in CO2 emissions covered by the scheme.

CORSIA was adopted in 2016 during the ICAO assembly by member States. By the end of the assembly, 65 States had already volunteered to implement the scheme from its outset, covering approximately 80 percent of CO2 growth in 2021-2035. The historic significance of this agreement cannot be overestimated. CORSIA is the first global scheme covering an entire industrial sector. The CORSIA agreement has turned years of preparation into an effective solution for airlines to manage their carbon footprint.

Q: How does IATA negotiate with local governments to promote the sector and facilitate operations?

A: To generate strong partnerships with governments is one of IATA’s top priorities. The airline industry is unique and we have found that by working closely with governments our industry is able to provide the most value. It is no surprise that where the industry is producing the most economic and social benefits — in places such as Panama and in the Gulf region in the Middle East — there is a close partnership between airlines and local authorities. When we work together our industry drives additional economic development, trade and job creation and of course more travel destinations and flight frequencies for air travelers.

Q: How does IATA determine the necessary measures to undertake for safety and environmental protection?

A: All IATA members must participate regularly in the IATA Operational and Safety Audit. The program is an internationally recognized and accepted evaluation system designed to assess the operational management and control systems of an airline. The total accident rate for IOSA carriers between 2011 and 2015 was 3.3 times lower than the rate for non-IOSA operators. As such, IOSA has become a global standard, recognized well beyond IATA membership.

You May Like

Most popular