Solid Auto Parts Performance Supports Economy

STORY INLINE POST

Q: What are the main drivers behind the growth of the Mexico’s auto parts industry?

A: Mexico’s auto parts industry grew between 4 and 5 percent in 2017 to a total value of US$87.7 billion. This includes production of auto parts for the domestic and expoting markets, including original equipment and the aftermarket. This result was possible thanks to US vehicle production reaching 12 million units, contributing to North America’s overall light-vehicle production of over 17 million units. In 2017, the Mexican automotive industry accounted for 20 percent of Mexico’s manufacturing GDP and 3 percent of the total GDP, with the auto parts industry accounting for half of these percentages. The Mexican auto parts sector is also responsible for the creation of 810,000 direct jobs in 25 states.

Q: How on track is Mexico to become the world’s fourth-largest auto parts manufacturer by 2020?

A: Mexico is on the right path. The country is only US$10 billion behind Germany in this sector. Increased production of vehicles in the US strengthens Mexico’s chances to reach this ranking, but rising interest rates in Mexico and the US can be a challenge. Higher interest rates mean consumers pay more each month for their car loans and they postpone replacing their vehicle or they go for less-equipped units. This reduces demand for some auto parts as OEMs produce fewer vehicles.

Q: How can Mexico continue promoting foreign investment in an uncertain business environment?

A: The country is making important advancements in manufacturing and R&D operations but there are issues that need to be addressed. Mexican labor needs to grow in quantity and quality as some regions face difficulties hiring enough employees capable of working on production lines. In terms of investment oriented to R&D, Mexico is competing with other emerging markets such as India, Eastern Europe, Brazil and China. These countries have quality engineers and competitive labor costs but unlike Mexico, their governments offer tax incentives to companies that do R&D. Mexico is missing out on the attraction of R&D centers because of the lack of similar incentives.

Q: What are the main challenges that Mexican companies face to become world-class suppliers?

A: While some Tier 1 companies merely supply their components to OEMs, others also collaborate with OEMs on technology development. There are five or six Mexican Tier 1 suppliers that fall into the second category and engage in technological advancements oriented to self-driving systems, electrification and other trends. Meanwhile, there are around 100 Mexican companies that supply directly to OEMs but do not break any technological paradigm in the automotive industry, which means there is still an opportunity for further growth.

Regarding international suppliers, these companies generally need to import semi-finished components and raw materials for their operations. This is the segment that could improve the most, either from a national-development or from a foreign-investment standpoint. Better programs are still needed to link international suppliers with the local supply chain, since foreign companies are often unaware of Mexico’s capabilities.

Q: How can North America grow its competitiveness in the global automotive market?

A: North America is a large importer of raw materials, automotive components and vehicles. Yet, its exports outside the region are low. The NAFTA market produces the vehicles it consumes rather than the vehicles that the world demands. On the contrary, Asia and Europe produce vehicles that cater to both their domestic demands and those of the rest of the world. North America is missing out on the opportunity to produce and export the compact and low-consumption vehicles that the rest of the world wants.

Q: How will the arrival of BMW, Mercedes-Benz and Toyota impact the local supply chain?

A: The arrival of new OEMs will lead to the construction of new auto parts plants and the expansion of production lines. Companies that came to San Luis Potosi and Aguascalientes to cater to BMW, INFINITI or Mercedes-Benz are already working on prototypes and components to start supplying these OEMs. BMW chose to set up shop in Mexico because of the German Tier 1 suppliers already in the country. Most of the suppliers opening plants in San Luis Potosi to cater to this OEM are not new to Mexico but have operations elsewhere in the country. Around 90 percent of the Top 100 global auto parts suppliers are present in Mexico. The rest are Chinese companies catering to the Chinese market.

Component manufacturers that have yet to set up shop in Mexico in the short to medium term will supply Toyota at its plant in Guanajuato, currently under construction. We expect the Bajio region will attract auto parts investments worth around US$300 million to support the region’s already-developed Japanese supplier base. The fact that Nissan, Honda and Mazda are present in the Bajio will help Toyota have a soft landing as most of the supplier base it needs is already there.

Q: Are Mexican automotive component suppliers ready to meet stricter requirements to service premium brands?

A: Mexican auto parts companies are more than ready to supply premium companies and have done it for a while now. Mexico’s auto parts competitiveness is based on the 17 million vehicles produced in the NAFTA market rather than on the 3 million produced in Mexico.

Mexico produces all the seatbelts used in North American vehicle production, including Cadillac, Mercedes-Benz and BMW. Even Tesla uses a variety of components produced in Mexico by Mexican companies. Rassini, for example, produces special braking pads that transform kinetic energy into electricity that charges Tesla’s electric-vehicle batteries. Mexican suppliers could face a greater challenge producing components for cheaper Chinese models than for premium vehicles.

Q: What new opportunities will the arrival of Korean and Chinese brands provide to local auto parts manufacturers?

A: These companies are not particularly open to new suppliers or technologies. Both Korea and China prefer to stick to their national suppliers. Still, it is just a matter of time before these companies follow the example of Japanese OEMs and start opening to local suppliers. When Kia and its suppliers arrived to Monterrey, they focused all their attention on building their assembly plants, developing the vehicle they would manufacture and training the staff they would employ. By the second generation of made-in-Mexico Kia vehicles, we will see greater participation of Mexican auto parts.

Entering the supply chain of a Korean manufacturer is challenging and the best strategy is to approach Kia’s and Hyundai’s purchasing departments in South Korea. Mexican components manufacturers need to go to Korea, present their manufacturing capacities and persuade Korean automakers to promote local joint ventures between Mexican companies and their traditional Korean suppliers.

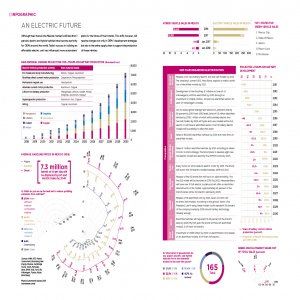

Q: What auto parts sectors will see their business grow once green vehicles conquer the roads?

A: An electric, self-driving vehicle will require fewer components than today’s cars and demand for parts such as electric harnesses will increase. An average internal-combustion vehicle requires around 1.5km of cable while an electric, self-driving vehicle will need between 3.5km and 4km. This increased demand is good news for Mexico as the country is a global leader in the production of electric harnesses for automotive applications. Furthermore, the most important manufacturers of sensors and electric motors are already present in the country. Commodities such as pistons will fade away and their manufacturers will have to migrate toward other components. We are only seeing the dawn of this migration.

Q: What are the main market challenges that electrified vehicles face?

A: Reaching mass-production of hybrid and electric vehicles will depend on the technology developed. As long as electric vehicles lack the average 500km of autonomy that today’s combustion engines offer and charging times similar to the 10 minutes it takes to fill a gasoline tank, it is unlikely that consumers will adopt them. Once electric models improve in both of these elements, consumers will change their mindset.

You May Like

Most popular