What Mexico’s New Storage Rules Really Mean for Decision‑Makers

STORY INLINE POST

By Ian de la Garza | CEO -

Fri, 07/25/2025 - 08:00

By Ian de la Garza | CEO -

Fri, 07/25/2025 - 08:00

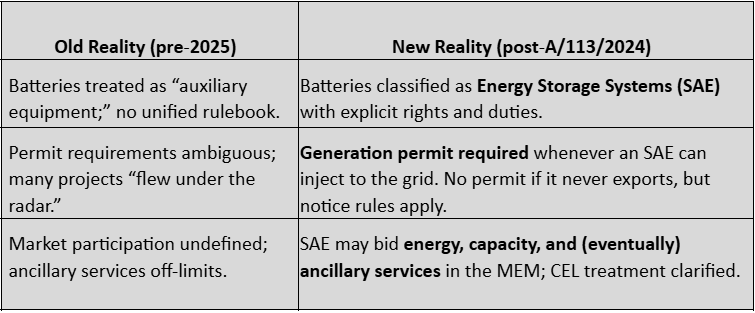

After years of stop‑and‑go drafts, Mexico’s Energy Regulatory Commission (CRE) finally published Resolution A/113/2024 in the Diario Oficial de la Federación on March 7, 2025. The resolution issued the General Administrative Provisions (DACG) that govern how Battery Energy Storage Systems (BESS, or SAE in Spanish) connect to – and interact with – the National Electric System. The rules became effective March 10, 2025.

For the first time, storage is no longer a regulatory afterthought. It now sits on the same legal footing as generation. That upgrade carries opportunity – new revenue streams, improved resiliency, tariff arbitrage – and new obligations, including permits, interconnection studies, and market compliance.

Big Picture: What the DACG Actually Do

Executive takeaway: Storage is now a regulated business line, not an accessory. That unlocks bankability – but only if you treat compliance like you would for a new power plant.

The Five Official Modalities – and Which One Fits You

The DACG define five flavors of storage. Pick the wrong one and you may trigger unnecessary permits – or worse, violate grid codes.

SAE‑CE — Tied to a Power Plant

Use‑case: Hybridizing a solar or wind farm to smooth intermittency, firm up capacity, or shift production.

● Permit: Existing generation permit must be modified (the addition is deemed a technical modification).

● Interconnection: New studies with CENACE; same Point of Interconnection.

● Market note: No extra CELs for stored energy; you must demonstrate that CEL‑eligible energy was produced by the plant, not the battery.

SAE‑CC — Behind the Meter at a Load Center

Use‑case: Industrial facility that wants peak‑shaving, tariff arbitrage, back‑up power, or to ride through grid outages.

● Permit: No generation permit as long as electricity is never exported.

● Notice: If connected at medium or high voltage, you must notify the CRE within 90 business days of commissioning (paperwork only, for statistics).

● Market option: You may register as a Qualified User and buy energy in the MEM, but still cannot inject.

SAE‑AA — Isolated Supply Schemes

Use‑case: Remote mines, island resorts, or legacy autoabasto grids aiming for diesel displacement.

● Permit: Treated as part of the isolated‑supply plant; generation permit (or authorisation) applies.

● Grid tie: None, by definition; import/export only under isolated‑supply rules.

SAE “Non‑Asociado” — Standalone Merchant Storage

Use‑case: Pure‑play storage developers providing peak‑shaving, frequency regulation, or arbitrage to the grid.

● Permit: Full generation permit required.

● Registration: Must register as a firm power plant and be represented in the Wholesale Electricity Market (MEM).

● Performance test: To count as firm capacity, you must prove at least three hours of uniform discharge capability (or meet the APD agreed in interconnection studies).

SAE‑GE — Distributed Generation ≤ 0.5MW

Use‑case: Small commercial rooftops adding a battery under the Generación Distribuida regime.

● Permit: Same simplified GD notice procedure (no full permit).

● Interconnection: Manual for DG plants < 0.5 MW still applies.

Key Compliance Milestones You Cannot Ignore

Already Have Solar? Your Migration Roadmap

1. Status Quo Protected: Existing PV systems may keep running exactly as they are; no retroactive battery mandate. Mondaq

2. Assess Your Contract Type:

○ Net Metering / Generation Asset PPA: Adding a battery usually triggers the SAE‑CE route → permit modification.

○ Behind‑the‑Meter Savings Contract: Battery likely falls under SAE‑CC → only notice, no permit.

3. Budget Realities: Industry experience shows adding a lithium‑ion package sized at 25‑30 % of PV output often boosts EPC capex by 20–30% – but financing costs may drop as financiers now have a clear legal framework.

4. Timeline Watch: Interconnection studies with CENACE can add six to eight months to the schedule; factor that into investor IRR models.

Market Opportunities CEOs Should Put on the Radar

Firming Renewable PPAs: Hybrid PV‑plus‑storage beats standalone PV in Time‑of‑Delivery PPAs and improves curtailment risk. Early movers can lock in premium prices before ancillary‑service tariffs reset the playing field.

Tariff Arbitrage and Demand Charges: With the DACG, behind‑the‑meter batteries are explicitly allowed to charge from the grid. Many medium‑voltage C&I users face demand charges that represent 40‑60% of their bill. A right‑sized SAE‑CC can shave 10‑15% off total energy costs without a generation permit.

Resilience as a Service: The rulebook recognises storage as a load‑center asset, enabling multihour backup for critical processes. CFOs can now capitalize Opex‑heavy diesel spend into a financed battery asset; insurers increasingly reward facilities with proven outage‑ride‑through capability.

Ancillary Services (2026+)

Once CENACE finalises the tariff and IT upgrades, standalone or hybrid SAEs can bid frequency regulation, spinning reserve, and black start – revenue streams largely untapped in Mexico.

Risk Matrix – What Keeps Bankers Awake

Implementation Playbook – Step‑by‑Step for Leadership Teams

1. Map Your Use‑Case to a Modality.

Assign a legal‑technical team to diagnose whether your project is SAE‑CE, CC, AA, Non‑Asociado, or GE. Misclassification is the No. 1 source of delay.

2. Commission a High‑Level Feasibility + Grid Impact Screen.

A three‑week desktop study costs a fraction of a formal CENACE study and spots fatal‑flaw interconnection issues.

3. Engage CRE Early.

Even SAE‑CC projects benefit from informal CRE pre‑filings to confirm that notice (not permit) is sufficient. Build four to six weeks into your Gantt.

4. Line Up Suppliers with Proven Mexican Track Records.

Grid‑code compliance (Protections, PQ, SCADA) is non‑negotiable; using unfamiliar PCS brands can derail the acceptance test.

5. Re‑Model Your PPA or Tariff Assumptions.

Update IRRs to reflect energy‑shifting spreads, capacity prices, and potential ancillary service upside.

6. Plan for Degradation and End‑of‑Life.

The DACG are silent on recycling, but SEMARNAT waste laws still apply; set aside CAPEXfor second life or disposal.

7. Build Optionality for Future Market Rules.

Design EMS and metering capable of real‑time dispatch so you don’t retrofit once ancillary markets open.

CFO Cheat‑Sheet: Numbers That Move the Needle

What Remains “To‑Be‑Written”

● Ancillary Service Tariffs: CRE’s 270‑day clock expires December 2025. Expect heated debates over cost‑based vs market‑based pricing.

● Grid Charging Protocols: Developers need clarity on state‑of‑charge requirements for reserve obligations.

● Interconnection Contract Templates: Without the new open‑access drafts, banks may insist on side letters; build that into legal timelines.

● Environmental and Recycling Guidelines: SEMARNAT has yet to publish lithium or LFP end‑of‑life rules; keep an eye on 2026 waste‑law amendments.

Strategic Questions for Your Next Board Meeting

1. Which modality positions us for both near‑term savings and future market upside?

2. How will storage reshape our hedging and procurement strategy over the next five years?

3. Do we internalize BESS on‑balance‑sheet, lease it, or structure a tax‑equity partnership?

4. What resilience value (measured in avoided downtime) justifies the CAPEX to operations?

5. How do the transitory deadlines align with our project pipeline – and what’s Plan B if they slip?

Bottom Line

Agreement A/113/2024 does not simply legalise batteries, it invites companies to rethink energy as a portfolio of flexible assets. For executives ready to move, the rules provide enough certainty to green‑light pilot projects today, while leaving room for lucrative ancillary revenues tomorrow.

Treat the new framework with the same rigor you would apply to a generation asset acquisition. Align finance, legal, operations, and sustainability teams early, and you will turn storage from an engineering curiosity into a board‑level profit center.

You May Like

Most popular