Harnessing the Value of SLP’s Mining Sector

STORY INLINE POST

Q: Which role has the mining industry played in the historic development of San Luis Potosi, and what have been the most important mining districts?

A: In the 1500s cities like San Luis Potosi, Guanajuato, Zacatecas, Parral and Pachuca developed following the mining activity that took place during the Colonial period. The conquistadores arrived via the Gulf of Mexico and made their way to the north of the country crossing the “Silver Route”. In San Luis Potosi evidence has been found of pre-Columbian mining, from the times of the Guachichil and Chichimeca civilizations in the District of Guadalcázar. Although the oldest mining district is Charcas, dating from 1584, the state’s most relevant discovery was Cerro San Pedro in 1592, located 6km from the closest water source, the Tangamanga valley, where the city was founded. Other relevant historic mining districts are Guadalcazar from 1609, Villa de Ramos from 1630, and the Salinas district, providing salt to the state’s plants.

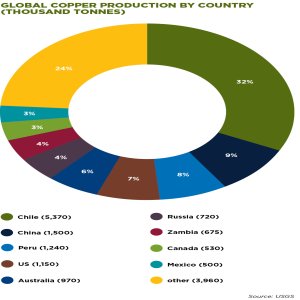

Q: What relevance does the state’s mining production have on the national scale?

A: In 2012 the state ranked sixth in the country, with its mining-metallurgic production valued at US$1.3 billion. Mexichem’s Las Cuevas mine is the largest fluorite mine in the world, making us the second biggest fluorite producer in the country. We rank third in copper production, with the Santa María de la Paz mine being the main producer, and third in zinc, with the Charcas mine from Grupo Mexico being the biggest producer. We occupy the sixth place for gold production, with New Gold’s Cerro San Pedro mine and Santa María de la Paz’s La Paz mine being the most relevant. The state ranks seventh in silver production, mainly produced from the central and the Altiplano regions. San Luis Potosi is also rich in non-ferrous minerals, such as gypsum, clay, stony materials and aggregates.

Q: How would you describe the current mining environment in the state, in terms of availability of land for exploration and the concessions market?

A: From the 6.2 million hectares in the state 25% are already under mining concessions, especially in the Altiplano region. In the Huasteca region, to the east, we find mostly non-ferrous mining, and stony terrain. Thanks to the area’s potential it is hard to find unexplored land. Canadian and American companies such as Newmont, Revolution, First Majestic, Cordillera, Endeavour, Goldcorp, and the largest Mexican companies such as Grupo Mexico, Peñoles and Minera Frisco already have a presence there.

Q: What are the incentives offered to the mining industry by the Directorate for Mining in order to encourage exploration?

A: We have played an important role in the national geological and infrastructure programs. In order to promote the state’s potential we have worked on its geological cartography, as well as the mineral resources inventory by municipality. We are among the states that have conducted mineral cartography most extensively, with 62% of the state’s surface having been covered at a scale of 1:50,000 – all of this was done with the support of the Mexican Geological Survey (SGM).

Q: How is the Directorate for Mining driving its efforts to continue developing the state’s mining potential?

A: In order to attract investment we work according to four strategic pillars, with promotion being the first. We aim to attract investment by promoting our state’s potential. Our second pillar is our technical and legal consultancy team, which is able to provide knowledge and expertise to the small and medium mining industry, while also looking after social practices. The third pillar is an updated online platform that shows all land availability. Thanks to our Mining Registry, and to the use of tools such as AutoCAD Map and other programs offered by MapInfo, we are able to show INEGI’s images and the current mining concessions in the state. Anyone requesting this information will have access to the SIAM, to the SGM’s online service, and to GeoInfoMex. The fourth pillar is making sure that all levels of the supply chain have access to technical and legal training programs, keeping close relationships with scientific and technological institutions such as IPICYT (San Luis Potosi’s Institute for Scientific and Technological Investigation) and with Universities such as UASLP (The Autonomous University of San Luis Potosi). We promote socially conscious mining and respect for the environment, with the objective of securing the state’s sustainable development.

You May Like

Most popular