Record Silver Price Surge Confirms Precious Metal's Critical Role

STORY INLINE POST

By Michael DiRienzo | Executive Director -

Tue, 12/09/2025 - 07:00

By Michael DiRienzo | Executive Director -

Tue, 12/09/2025 - 07:00

(The Silver Institute is pleased to provide this update on the 2025 global silver market. We presented our thoughts at the Annual Silver Industry Dinner in New York City in November.)

This has been a dramatic year for the silver market, with record metal prices, an unprecedented liquidity squeeze resulting in record-high lease rates, record volumes delivered into CME vaults reflecting tariff concerns in the United States, and silver officially designated as a critical mineral by the US government. These developments coincide with elevated macroeconomic and geopolitical risks, including US trade policy, prompting investors to lift allocations to precious metals for portfolio diversification. As a result, investment demand has strengthened noticeably, comfortably offsetting the weakness across all key silver demand areas.

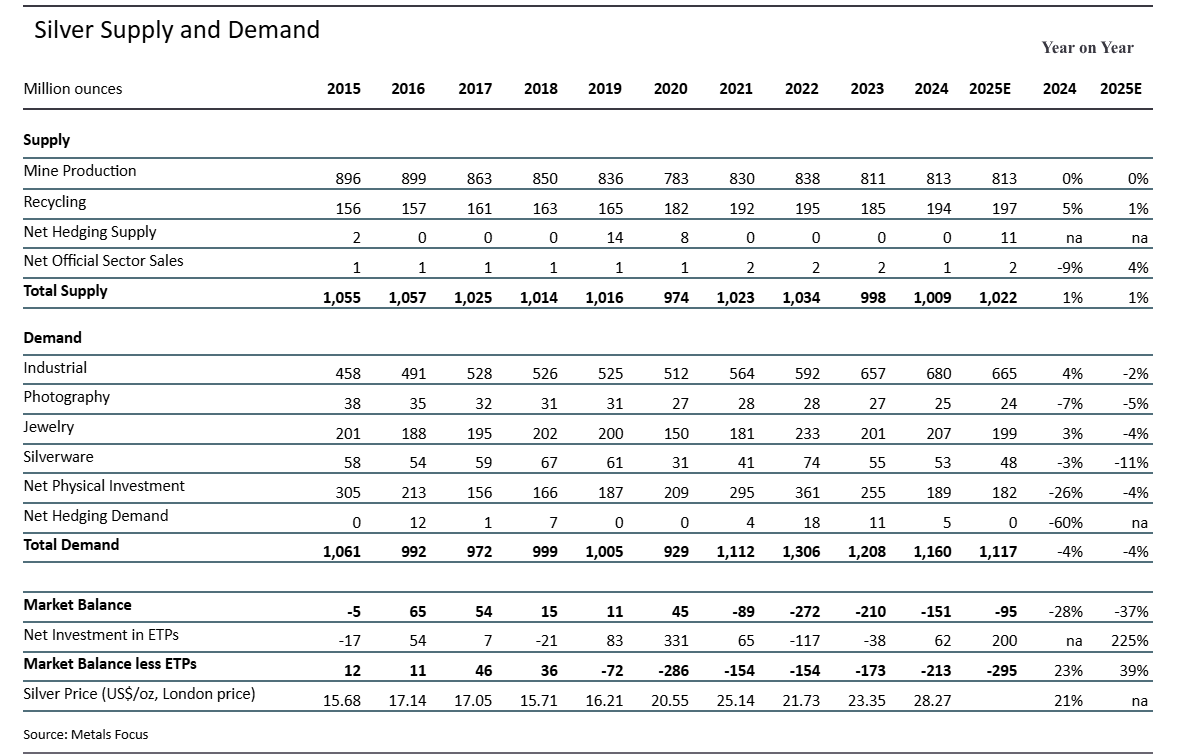

Against this backdrop, the silver price hit a record high and posted an astonishing year-to-date gain of 95%+ on Dec. 1. This eclipses the 62% rise for gold and the 16% increase for the S&P 500. In terms of market fundamentals, global supply is estimated to rise by 1%, underpinned by a modest return to producer hedging. Global demand is expected to decline by 4%, with all significant demand categories posting lower totals. Even so, the market has remained in deficit in 2025, marking the fifth consecutive year.

The following are the key highlights from the presentation:

The silver price hit a record high of US$57.85 on Dec. 1. Silver has held mainly above US$47, a sign of underlying market strength. Since peaking in April at over 107, the gold:silver ratio has trended lower, falling to 78 in October, its lowest since July 2024, suggesting increasing institutional investor confidence in silver.

Exchange-traded product holdings are up by roughly 18% to Nov. 6, generating a year-to-date rise of 187Moz. This reflects investor concerns over stagflation, the Federal Reserve’s independence, government debt sustainability, the US dollar’s role as a safe haven, and geopolitical risks. Silver’s exceptional price performance and its favorable supply-demand backdrop have further reinforced investor confidence. Roughly half of silver-backed ETPs are held in London, which contributed to October’s liquidity squeeze.

Global silver demand is expected to drop by 4% year-over-year (y/y) to 1.12 billion ounces in 2025. All key areas of silver demand are on course to post losses, led by industrial demand, jewelry, bar and coin demand.

Industrial demand is forecast to decline by 2% in 2025 to 665Moz. This reflects the impact of global economic uncertainty stemming from tariff policies and geopolitical tensions, as well as a more rapid pace of thrifting due to soaring silver prices. In photovoltaics (PV), global installations are set for a new record high. However, due to a sharp drop in the amount of silver used in each module, PV silver demand is forecast to ease by around by 5% y/y. This outcome will be partially offset by healthy gains in the AI market for data centers, and further growth in electric vehicle sales (albeit more modest than previously expected).

Silver jewelry and silverware are expected to decline by 4% and 11%, respectively, this year. For each segment, this largely reflects weakness in India, where the rupee silver price has been trading at record highs, well before the international market followed suit.

Bar and coin demand is forecast to decline by 4% to a seven-year low of 182Moz in 2025. This is a result of weakness in the US market, which is offsetting gains in the other key markets of India, Germany, and Australia. Despite a recent uptick in US demand, for much of 2025, the United States has had to contend with sizable retail investor liquidations. In contrast, Indian investors have bought into rising local prices, expecting further upside in 2025.

In 2025, global mined silver supply is expected to remain flat y/y at 813Moz. Higher Mexican and Russian production will be offset by lower output in Peru and Indonesia. Primary silver supply is forecast to rise 3Moz y/y to 227Moz, accounting for 28% of global output. Mexican production is predicted to rise 5Moz y/y to 186Moz, supported by the restart of Peñoles’ Tizapa following a prolonged labor strike, the ongoing ramp-up at Endeavour Silver’s Terronera, and higher output at Southern Copper. The average all-in sustaining cost (AISC) for H1.25 fell 9% y/y to $13.0/oz, its lowest since H1.22, as lower operating costs offset the rise in royalties and taxes. AISC margins rose, supported by a higher silver price, reaching $19.7/oz in the same period, the highest in over a decade.

Recycling this year is expected to rise by just 1% but still achieve a 13-year high. The increase reflects higher recycling of silverware, especially in western markets, which offsets a slightly weaker tone to industrial scrap supply.

Overall, 2025 will see the fifth successive deficit; albeit lower y/y, it is still estimated at a sizeable 95Moz. For 2021-25, this results in a cumulative deficit of almost 820Moz. This helps to explain some of the market tightness this year.

This year has been exceptional for silver, especially given the ongoing structural market deficit, now in its fifth year, which is projected to continue into 2026. The ongoing global drive to clean energy solutions is a significant positive for silver, as it is widely used in photovoltaics, electric vehicles and their infrastructure, wind and nuclear energy, among others.

The proliferation of data centers, used to power artificial intelligence, is a net positive for silver, as their energy requirements will rely on silver and other metals.

You May Like

Most popular