Subsidy or Sun: How CFE Could Reduce Billions in Spending

STORY INLINE POST

By Ian de la Garza | CEO -

Tue, 09/30/2025 - 08:00

By Ian de la Garza | CEO -

Tue, 09/30/2025 - 08:00

Talking about electricity tariffs in Mexico is talking about finance: household finance and the state’s. In recent years, the government has softened the true cost of electricity with a broad subsidy on Tarifa 1 (and its climate variants 1A–1F). That contains perceived inflation for families, but implies a substantial public outlay, and, for high-consumption homes, the dreaded DAC tariff (High Domestic Consumption) appears as a reminder that subsidies at least have a limit. In parallel, distributed rooftop solar has taken off as a relief valve: it brings many users back down from DAC to 1C or 1D and, along the way, reduces pressure on subsidies. In this piece, with recent figures, I explain why rooftop solar is already a financial solution for 1C and 1D consumers and a fiscal strategy for Mexico. (CFE)

During 2019–2024, CFE received MX$523 billion (US$28 billion) in subsidies to keep residential tariffs below cost, 97% more than the previous six-year period. That figure not only shows the scale of the policy, it also illustrates its opportunity cost: every peso used to cheapen power is a peso not invested in productive projects, transmission, or healthcare.

The subsidy’s logic is social and reasonable because it protects basic consumption, but its broad design creates inequity (it also benefits households that don’t need it) and budget rigidity. In 2022, for example, at least MX$73 billion was allocated to electricity subsidies, making it the fourth-largest subsidy program in the federal budget. The inertia of these amounts explains why any alternative that reduces demand at peak hours or in hot regions has real fiscal effects.

Official discourse has recognized the annual scale of support — tens of billions, with estimates around MX$100 billion per year, confirming the magnitude of the “cushion” currently propping up Tarifa 1. The debate isn’t whether to support or not, but how to support better and how to spend fewer pesos per subsidized kWh.

How Tarifa 1 Works

Mexico defines seven residential sub-tariffs (1, 1A … 1F) with different consumption limits depending on climate. If your 12-month average monthly consumption exceeds your zone’s High Consumption Limit (LAC), CFE reclassifies you to DAC and you lose the subsidy. Official LACs are: 250 kWh/month (1), 300 (1A), 400 (1B), 850 (1C), 1,000 (1D), 2,000 (1E) and 2,500 (1F).

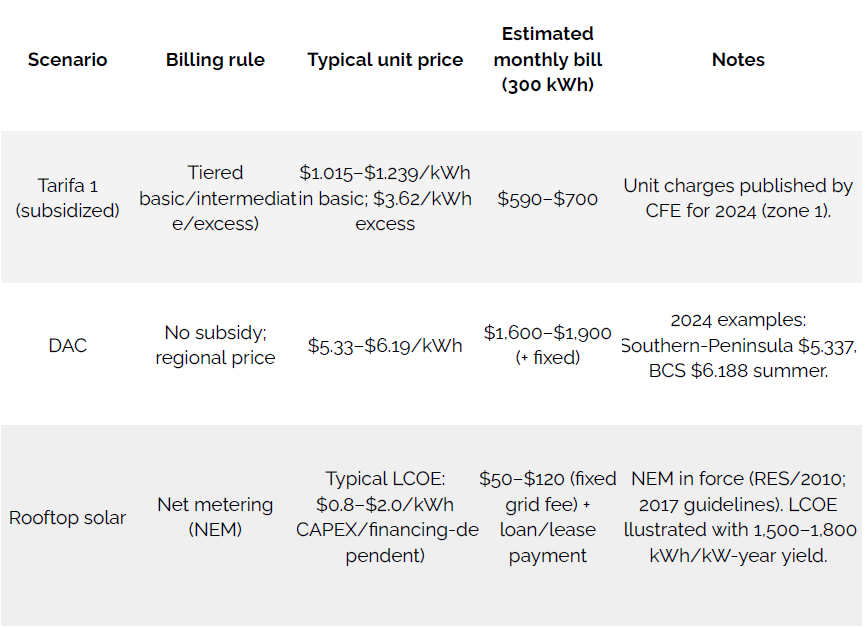

What hurts isn’t just losing the discount, but the price jump. In 2024, subsidized Tarifa 1 kWh ran MX$1.015–$1.239 in basic/intermediate blocks and MX$3.62 in excess (zone 1), while DAC kWh averaged MX$5.3–MX$6.2 depending on region. In the Southern-Peninsula zone, for example, MX$5.337/kWh in Feb 2024; in Baja California Sur, MX$6.188/kWh in summer. The gap is decisive for any ROI analysis.

Pocket translation: the real prize is tier-shaving in 1C/1D.

For most households in 1C and 1D, the biggest, fastest savings don’t come from “escaping DAC”; they come from pushing kWh down from the expensive tiers (excess) into intermediate or basic blocks. Think of it as trimming the peaks: a small 2–5 kW rooftop system sized to your seasonal highs can keep your 12-month average and your hottest months inside subsidized bands, where each kWh costs a fraction of the excess block. In practice, every kWh you self-generate during peak days often replaces one of the most expensive kWh on your bill, so the marginal ROI per kWh is high even if you never touch DAC.

How Under-Penetrated is 'Tier Optimization' Solar in 1C/1D?

Rooftop PV adoption has grown quickly, but the overlooked gap is right in 1C/1D: modest arrays that surgically shave the excess tier remain far from saturated. This is a different design brief than “full-offset” or “DAC escape.” It prioritizes marginal economics targeting the top 100–300kWh of your bill where the tariff steps up so paybacks stay attractive with smaller CAPEX, lighter roofs, and simpler interconnections. In hotter regions, a calibrated array that clips late-afternoon A/C peaks can keep families consistently in basic/intermediate blocks, compounding savings as the 12-month average stabilizes. For utilities and public finance, scaling thousands of these right-sized, tier-shaving systems in 1C/1D cuts subsidized kWh where they’re most costly, a fiscally smarter first mile than aiming only at DAC exits.

Finance Cases

Financial mechanics: Every kWh you produce on your roof is a kWh you don’t buy from CFE. If you’re in DAC today (kWh at MX$5.3–MX$6.2), every solar kWh “saves” you that price. Plus, by lowering your average below the LAC (for example, 850kWh in 1C or 1,000kWh in 1D), you regain the subsidized tariff for the rest of your grid consumption. It’s a double benefit: you save now and improve your future price.

● Scenario – 1D home (Monterrey). Historic use: 900 kWh/month near LAC. With 4.5–5 kW of solar, the home avoids falling into DAC during summer and stabilizes payment in subsidized blocks (basic + intermediate + excess 1D). Typical savings 45–60% versus no-solar, better when paired with efficiency (inverter A/C). (Own calc with 2024 reference tariffs.)

Technical key: With Mexico’s irradiance, a residential system yields ~1,500–1,800kWh/kW-year (varies by city and orientation). That performance means the levelized cost (LCOE) of rooftop solar competes with subsidized tariffs and is far below 1D, 1C.

FIDE’s Role and SENER’s 25% Subsidy: A bridge for 1C/1D/1E/1F Homes

“Paneles Solares para tu Casa” has been running since 2020: SENER covers 25% of system cost and FIDE finances the remaining 75% at a preferential rate (up to five years). The program is targeted to extreme-climate zones (tariffs 1C, 1D, 1E, 1F), with income/property requirements, promising up to 90% bill savings for eligible homes. As of April 2025, it reports 1,222 installations (~5.18MW), 8GWh/year generated, and a continuation of the incentive during heating season.

This design removes the “down-payment” barrier: the household doesn’t pay 100% of CAPEX up front, it “pays” the system with part of the savings, similar to a green mortgage on your own roof. For 1C/1D homes at DAC risk due to air conditioning, FIDE turns “it makes sense, but I lack liquidity” into “it makes sense and I do have access.”

What CFE Has (and Hasn’t) Done

Between 2019–2024, CFE’s public-facing role in rooftop solar for on-grid households was largely procedural: interconnection processing, bidirectional metering and service continuity. It hasn´t run a national program to mass-finance or mass-install panels for Tarifa 1 (1C/1D) users, and the first direct initiative with installations at scale only surfaced in 2025 through Sol del Norte, a geographically targeted pilot with free systems for a limited number of homes.

Several factors help explain the gap: (1) mandate and regulatory scope for the basic supplier, (2) capital prioritization toward networks and generation assets, and (3) a private market already offering financing, guarantees and installation capacity. In parallel, according to industry conversations and internal explorations referenced by stakeholders, CFE evaluated a large-scale financing program for subsidized residential tariffs, but it was not approved. Even without official publication, the direction of travel is clear: CFE has the data, billing rails and customer reach to catalyze demand-side savings quickly if the model is well designed.

Why Try Again, and At Scale?

- Fiscal leverage: Right-sized rooftop systems that keep 1C/1D users in basic/intermediate blocks reduce the most expensive subsidized kWh first, stretching public pesos further.

- Grid relief where it matters: Targeting late-afternoon peaks in hot zones lowers local stress and capacity needs without waiting for long-lead infrastructure.

- Use existing rails: CFE’s billing system can support on-bill financing/repayment, minimizing friction and default risk while crowding in private capital.

- Complement, not displace: A utility-anchored program can coexist with private installers/financiers, setting quality standards and de-risking credit, while the market executes.

The pragmatic path is a blended model: CFE sets the framework (eligibility, on-bill mechanisms, verification of savings), FIDE and private lenders provide capital, and private EPCs deliver. Start in 1C/1D high-heat municipalities, size systems to shave excess tiers, and measure success by subsidy pesos avoided per kW. If pilots confirm the unit economics, scale nationally with transparent KPIs.

Cost Comparison: Subsidized Tariff vs. DAC vs. Rooftop Solar

Comparable assumptions

Monthly consumption: 300kWh. Location: Tarifa 1 reference or regional DAC.

Excludes climate adjustments and VAT/fixed charges unless noted.

Quick financial read

- Versus Tarifa 1 (heavily subsidized), solar already competes on $/kWh,(payback depends on displacing expensive tiers/avoiding DAC).

- Net metering remains critical, backed by 2010/2017 regulation with enough stability to underwrite 15–20-year projects.

What Does It Cost to Install? (And Why ROI Is So Attractive)

Residential tickets vary by city and size, but 3–6kW systems commonly land in the MX%$70,000–$150,000 installed range, with published offers for 5kW around MX$95,000–MX$120,000 depending on equipment and warranties. For DAC homes, annual “avoided” spend is often MX20,000–MX$35,000 for mid-use households, yielding 3.5- to six-year paybacks even with financing. (Illustrative ranges from public quotes and price lists; exact figures depend on CAPEX, irradiance, local tariff, and usage habits.)

Implications for Public Policy and Private Strategy

For Finance Ministry/SENER: Every system that prevents DAC or brings 1C, 1D down to high subsidy basic or intermediate blocks. saves future subsidies and defers summer grid investments. Targeted programs (FIDE, Rooftop initiatives) that leverage private capital (leasing/credit) multiply fiscal impact per peso deployed. Measuring this pesos of subsidy avoided per kW installed should be an energy policy KPI for 2025–2030.

For CFE: DG is already critical mass (4.45GW) and grows where tariffs hurt most. Integrating it with metering, protection, and local dispatch cuts losses and marginal costs at peaks. Transparent interconnection timelines and clear NEM rules will keep the cost of capital low across the ecosystem.

For residential solar firms, the next growth market is 1C/1D with FIDE+finance bundles and corporate programs deploying hundreds of rooftops via platforms.

Solar as Fiscal Policy (Not Just Energy Policy)

Viewed through a financial lens, the Tarifa 1 subsidy is recurring spend that buys time — acceptable in emergencies, expensive as a permanent policy. Distributed solar, by contrast, is capex that reduces or avoids that spend over time. With net metering and right-sizing, payback arrives in 3.5 to six years and tariff protection lasts decades. For the state, targeted, leveraged programs (FIDE/SENER 25%, rooftop initiatives) buy future kWh at a fraction of the fiscal cost of subsidies. The value lies in focalization: support first where eliminating one kWh costs the most (DAC/1F/1D in summer) and where public investment crowds in private capital.

Mexico has sun to spare. What we must optimize is how we finance the rooftop transition: fewer pesos to broad discounts, more pesos to cut demand where it hurts. That’s how electricity bills — and public finances — stop burning every summer.

Key references (selected)

- Subsidies 2019–2024: MXN 523B (+97% vs. prior six-year). México Evalúa

– Números de Erario. (Números de Erario)

- Tariff scheme and LAC (1–1F) / DAC unsubsidized: CFE. (CFE Portal)

- 2024 unit charges (1/1A/1F) and 2024 DAC range by region: Infobae

(CFE amounts); Campeche Gov.; W Radio. (infobae)

- DG 2024: 106,934 new contracts; 4,447.92 MW cumulative; leading states. PV magazine México; Energía a Debate. (PV Magazine Mexico)

- NEM / regulatory framework: DOF (2010; RES/054/2010); 2017 DG guidelines (RES/142/2017). (Diario Oficial de la Federación)

- FIDE + SENER 25% / results: FIDE (2025 bulletin); SENER-FIDE microsite. (FIDE)

- CFE & panels (clarification): CFE 2024 bulletin; pv magazine México. (CFE Portal)

- “Sol del Norte” (Mexicali 2025): Energía Estratégica; Energy & Commerce. (Energía Estratégica)

- Bright (leasing; 4,700 customers; Series C US$31.5m): BusinessWire; Canary Media. (Business Wire)

- Solfium (2× revenue; Scotiabank; CO₂ with México2): BetaKit; Mexico Business News note; pv magazine México. (BetaKit)

- Mexico solar resource (GHI): Global Solar Atlas. (Global Solar Atlas)

![]()

Most popular